Business briefing Financial analysis Investing Money News Technology news Online Crypto Casino – Der Casino-Check 2025 Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Bitget Wraps Up Anti-Scam Month with Over 65% of Participants Successfully Identifying Crypto Fraud Tactics Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Crypto Casinos – Online Casino test winner 2025 Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Crypto Online Casino – Top online gambling platforms 2025 Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Bitcoin whales are increasing because long-term holders reach an all-time high Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Crypto Casino – The Great Online Casino Guide 2025 Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Crypto is becoming a bank – and Europe moves down Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news Crypto Valley records growth of 14% despite competition Jayd Johnson 3 July 2025 0

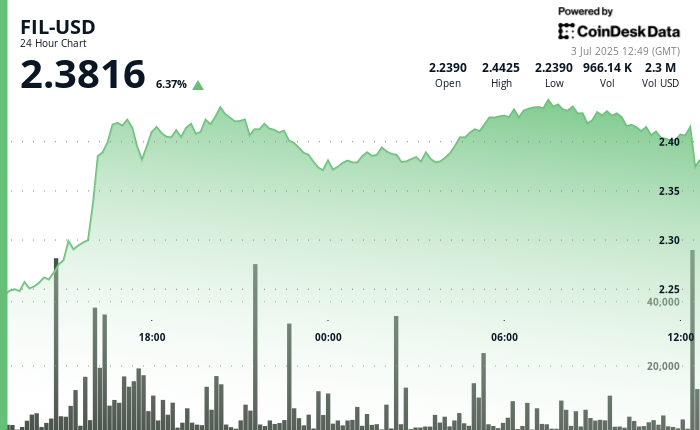

Business briefing Financial analysis Investing Money News Technology news Filecoin (Fil) increases up to 9 % in the course of the wider rally on the cryptom market. Jayd Johnson 3 July 2025 0

Business briefing Financial analysis Investing Money News Technology news New MacOS Shadcode “Nimdoor” attacks web3 and crypto platforms – ITOPNEWS.de Jayd Johnson 3 July 2025 0